Your personal credit score shows your history of borrowing and repaying money on a personal level. It’s used by lenders to assess your financial reliability, particularly if your business is new or doesn’t have much credit history.

What Is a Business Credit Score?

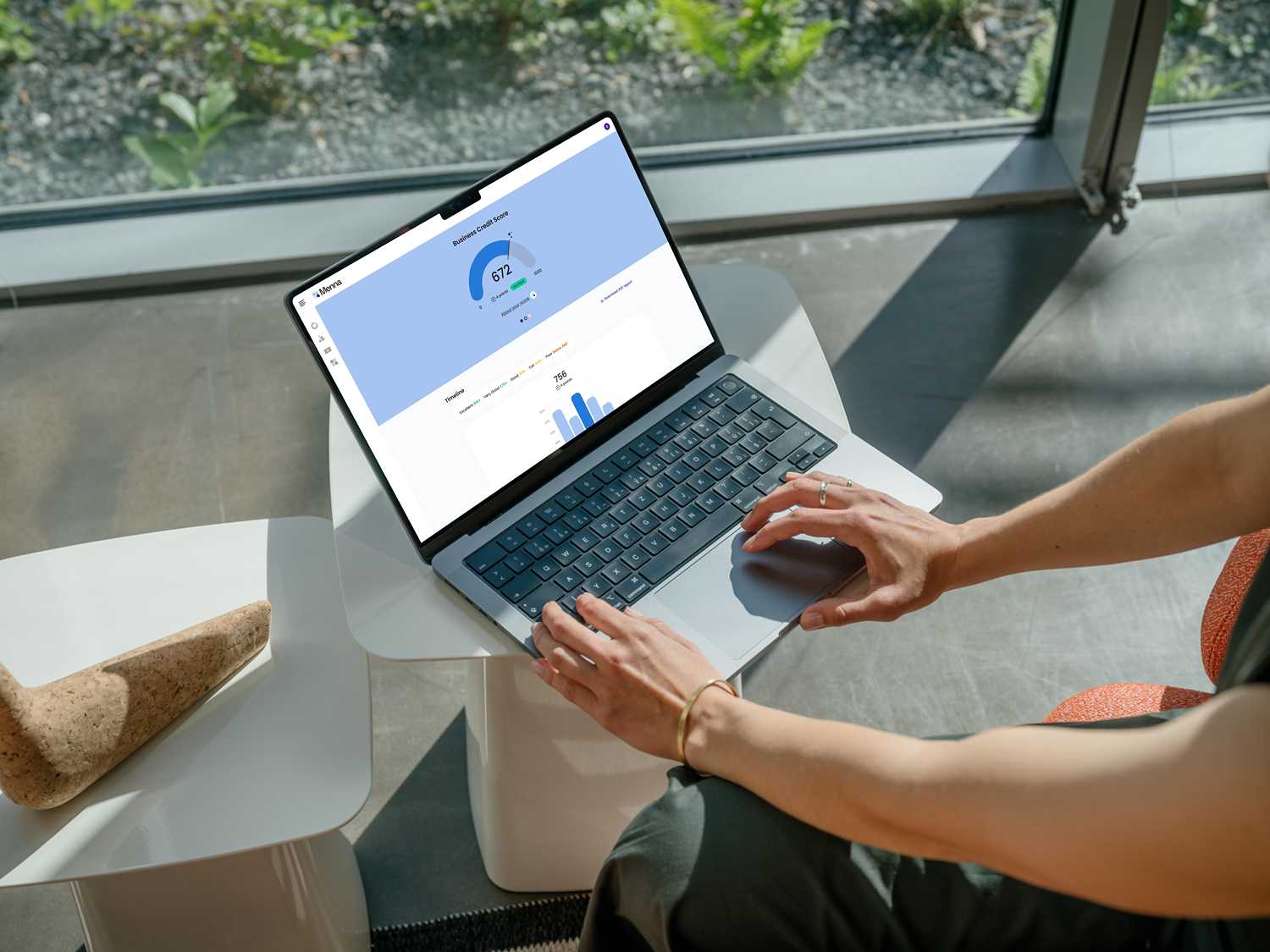

A business credit score reflects your company’s financial trustworthiness. It’s based on your business’s payment history, public records, and credit information from suppliers and lenders. Menna uses Equifax business credit data to help you check your score.

How Do Personal and Business Credit Scores Affect Loan Applications?

When you apply for business loans, overdrafts, or credit, lenders often check both your personal and business credit scores. A weak score in either area can impact your chances of approval or the terms you’re offered.

Why Does Personal Credit Matter for Your Business?

Many small businesses, especially sole traders and start-ups, are financially linked to their owners.

Lenders may look at your personal credit to decide if you can personally cover repayments if the business struggles.

Personal credit history can act as a guarantee when applying for business credit.

How to Build Both Your Business and Personal Credit Scores

Separate personal and business finances with a dedicated business bank account.

Pay all bills and credit repayments on time.

Use credit responsibly — on both personal and business credit cards or loans.

Regularly check your business credit score with Menna and monitor your personal credit through services like ClearScore or Experian.

Manage Both Scores to Boost Your Funding Chances

Understanding the difference between business credit scores and personal credit scores — and managing both — is vital to getting the best finance deals. Menna makes it easy to check your business credit score and helps you build a strong financial profile.

Lenders often check your personal score, especially if your business is new or you’re a sole trader. It helps them assess overall risk and repayment ability.